R&D Blog

Profit-Taking: Perry Kaufman | Trading Strategy (Test Period 2)

I. Trading Strategy

Developer: Perry Kaufman. Concept: Profit-taking improves performance. Source: Kaufman, P. J. (1995). Smarter Trading: Improving Performance in Changing Markets. New York: McGraw-Hill, Inc. Test Period 2: 2000-2011. Specification: Table 1. Results: Figure 1-2. Trade Setup: Long Trades: Exponential Moving Average turns up (EMA[i] > EMA[i − 1] & EMA[i − 1] < EMA[i − 2]; Index: i ~ Current Bar). Short Trades: Exponential Moving Average turns down (EMA[i] < EMA[i − 1] & EMA[i − 1] > EMA[i − 2]; Index: i ~ Current Bar). Trade Entry: Long Trades: A buy at the close is placed when the Exponential Moving Average turns up (bullish setup). Short Trades: A sell at the close is placed when the Exponential Moving Average turns down (bearish setup). Trade Exit: Table 1. Portfolio: 42 futures markets from four major market sectors (commodities, currencies, interest rates, and equity indexes). Data: 11 years since 2000. Testing Platform: MATLAB®.

II. Sensitivity Test

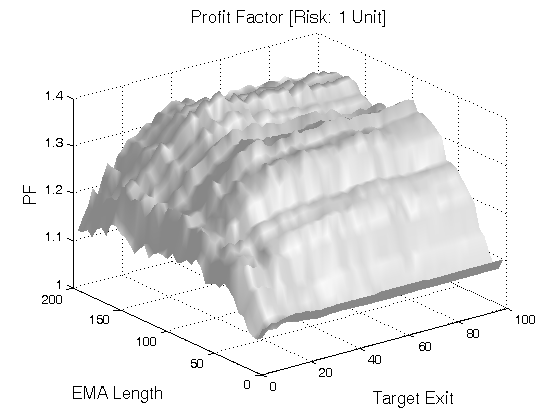

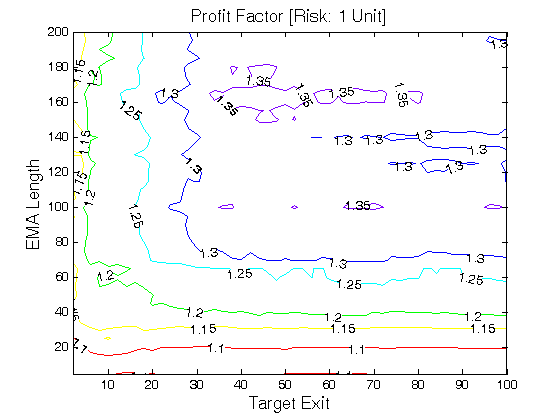

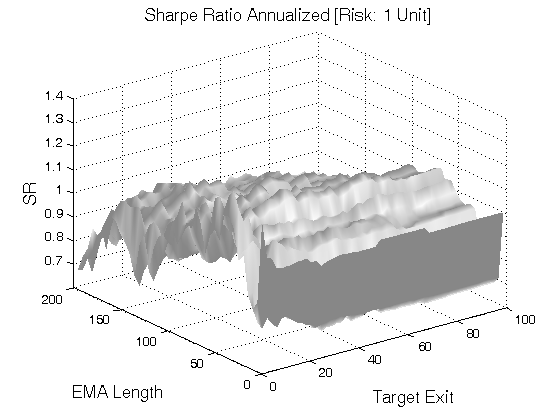

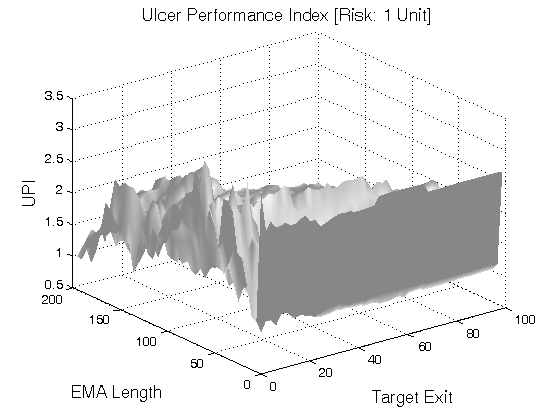

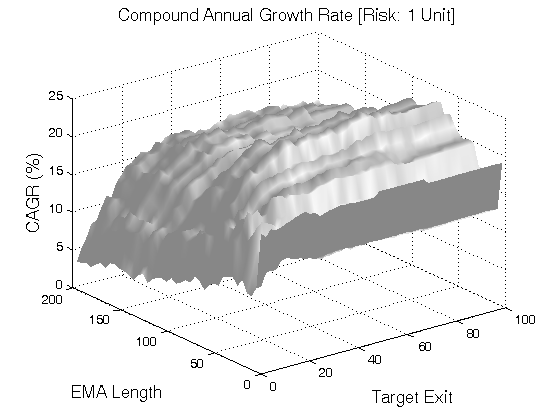

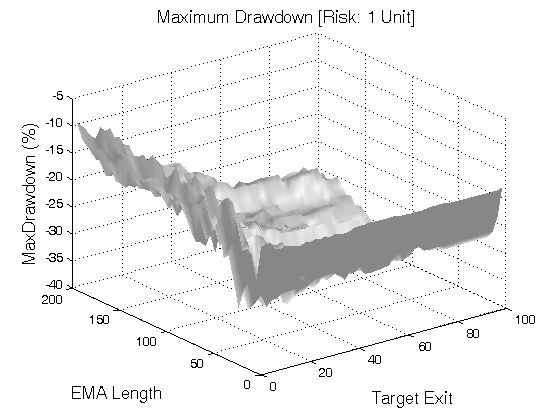

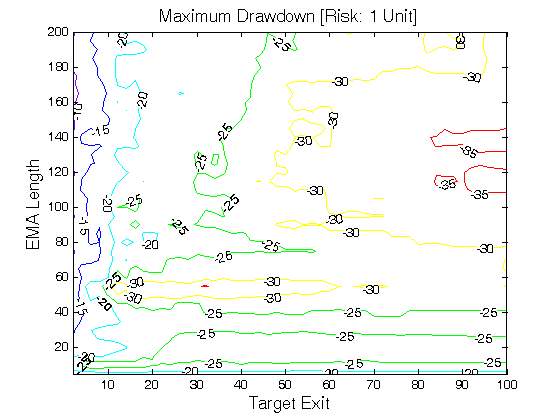

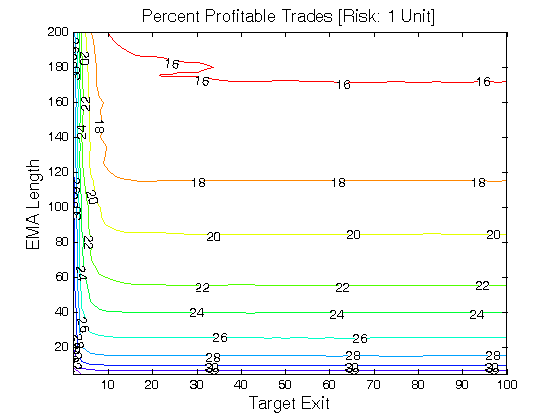

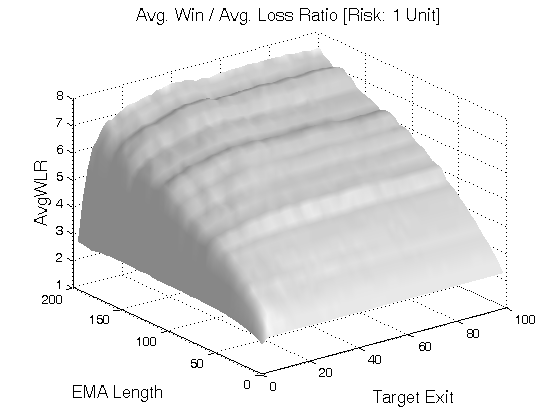

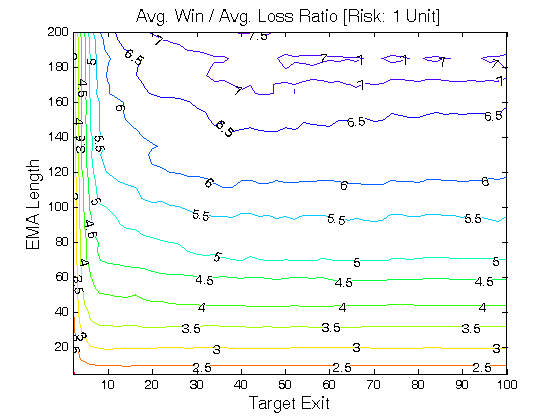

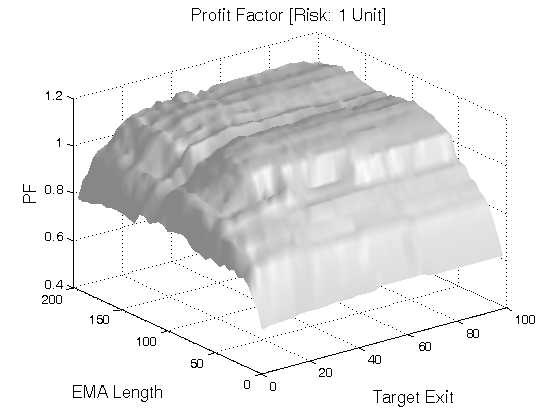

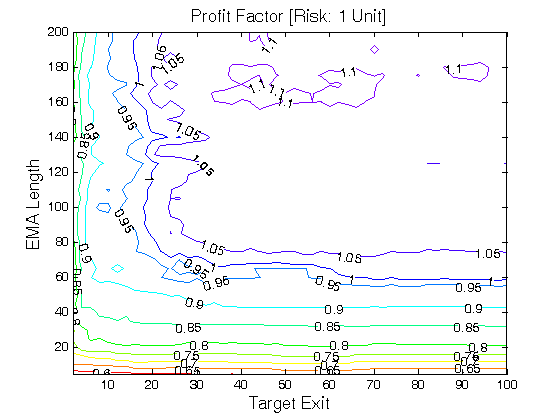

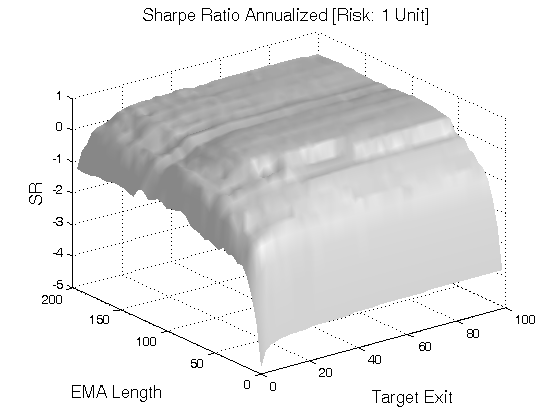

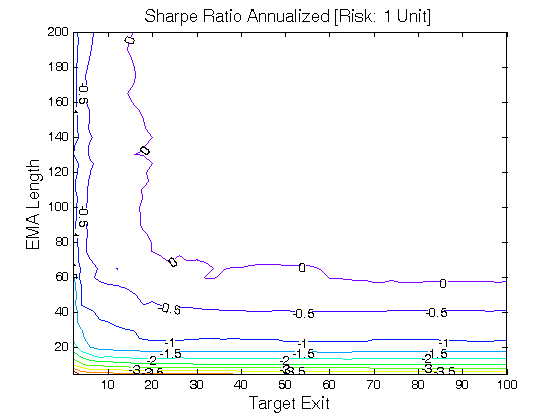

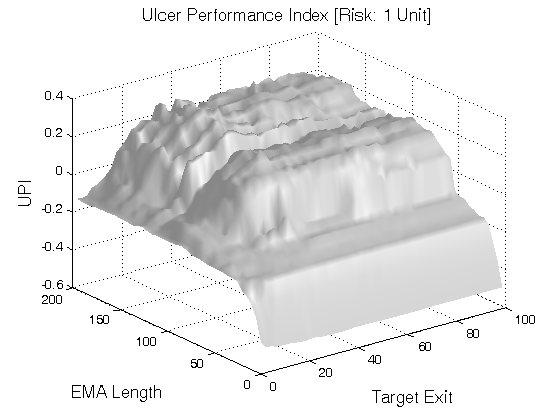

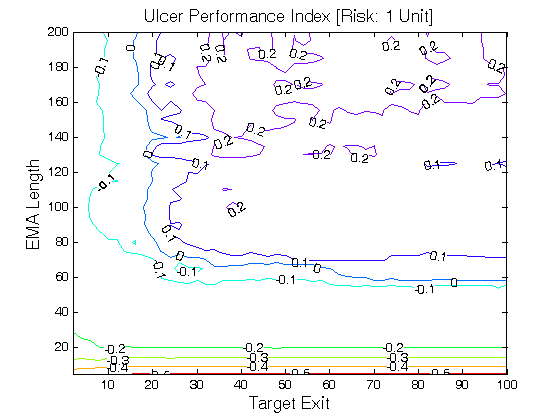

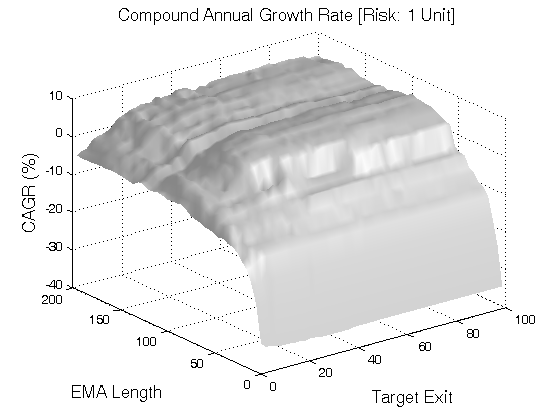

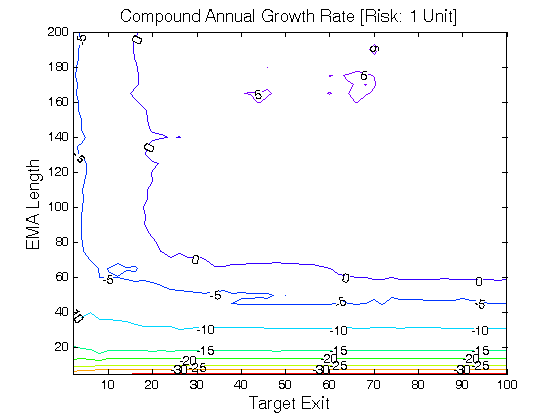

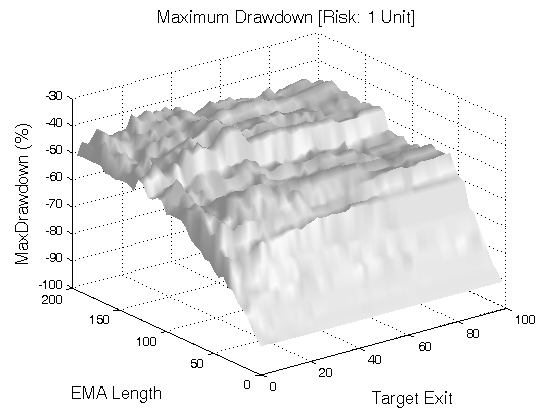

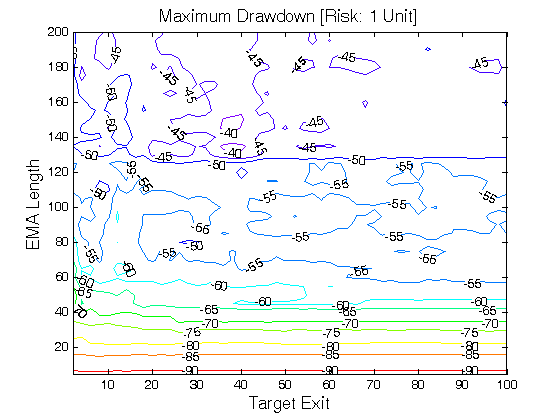

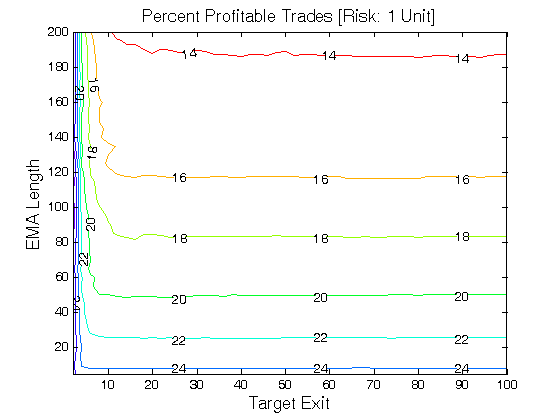

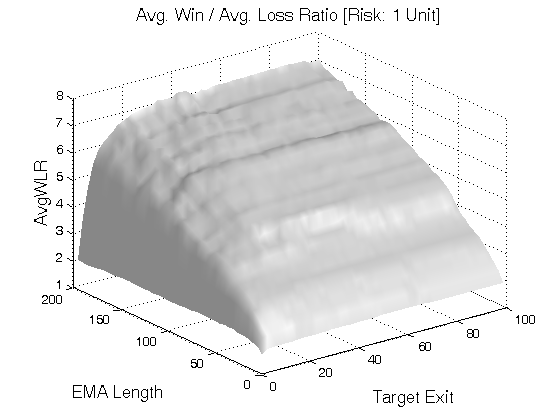

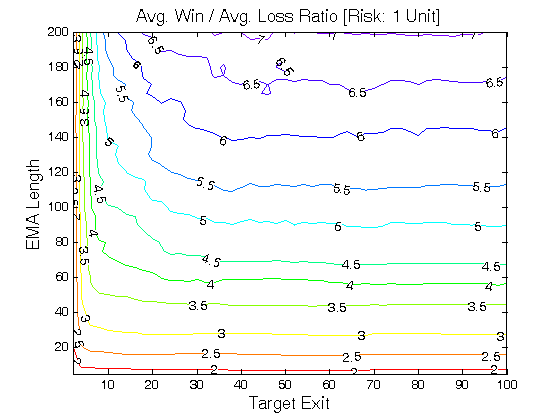

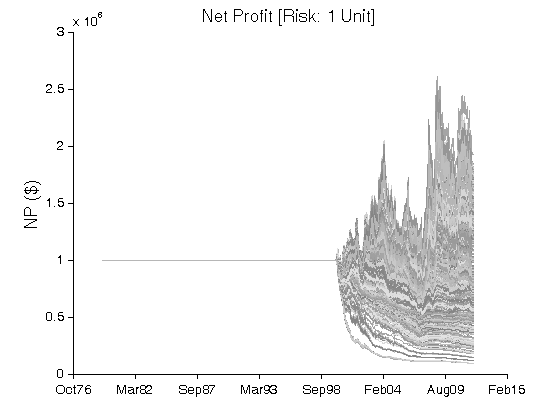

All 3-D charts are followed by 2-D contour charts for Profit Factor, Sharpe Ratio, Ulcer Performance Index, CAGR, Maximum Drawdown, Percent Profitable Trades, and Avg. Win / Avg. Loss Ratio. The final picture shows sensitivity of Equity Curve.

Tested Variables: EMA_Length & Target_Exit (Definitions: Table 1):

Figure 1 | Portfolio Performance (Inputs: Table 1; Commission & Slippage: $0).

| CONCEPT | SPECIFICATION | PARAMETERS |

| Auxiliary Variables: | EMA(EMA_Length) is the Exponential Moving Average over a period of EMA_Length. EMA[i] = EMA[i − 1] + α*(Close[i] − EMA[i − 1]), α = 2/(EMA_Length + 1). Index: i ~ Current Bar. | EMA_Length = [5, 200], Step = 5; |

| Setup: | Long Trades: EMA[i] > EMA[i − 1] & EMA[i − 1] < EMA[i − 2]; (Exponential Moving Average turns up). Short Trades: EMA[i] < EMA[i − 1] & EMA[i − 1] > EMA[i − 2]; (Exponential Moving Average turns down). Index: i ~ Current Bar. | |

| Filter: | N/A | |

| Entry: | Long Trades: A buy at the close is placed when the Exponential Moving Average turns up (bullish setup). Short Trades: A sell at the close is placed when the Exponential Moving Average turns down (bearish setup). | |

| Exit: | Target Exit: Long Trades: A sell at the close is placed if Close ≥ Upper%Target, Upper%Target = Entry*(1 + Target_Exit/100). Short Trades: A buy at the close is placed if Close ≤ Lower%Target, Lower%Target = Entry*(1 − Target_Exit/100). Stop Loss Exit: ATR(ATR_Length) is the Average True Range over a period of ATR_Length. ATR_Stop is a multiple of ATR(ATR_Length). Long Trades: A sell stop is placed at [Entry − ATR(ATR_Length) * ATR_Stop]. Short Trades: A buy stop is placed at [Entry + ATR(ATR_Length) * ATR_Stop]. | Target_Exit = [2, 100], Step = 2; ATR_Length = 20; ATR_Stop = 6; |

| Sensitivity Test: | EMA_Length = [5, 200], Step = 5 Target_Exit = [2, 100], Step = 2 | |

| Position Sizing: | Initial_Capital = $1,000,000 Fixed_Fractional = 1% Portfolio = 42 US Futures ATR_Stop = 6 (ATR ~ Average True Range) ATR_Length = 20 | |

| Data: | 42 futures markets; 11 years (2000/01/01−2011/12/31) |

Table 1 | Specification: Trading Strategy.

III. Sensitivity Test with Commission & Slippage

Tested Variables: EMA_Length & Target_Exit (Definitions: Table 1):

Figure 2 | Portfolio Performance (Inputs: Table 1; Commission & Slippage: $100 Round Turn).

IV. Conclusion: Profit-Taking

Simple profit targets reduce absolute returns and risk-adjusted returns (Portfolio: 42 US futures; Test Period 2: 2000-2011). This finding contradicts the conclusion of Perry Kaufman who made the test on a small sample of data (Portfolio: 3 markets; Test Period: 1988-1993). Perry Kaufman (1995):

[…] taking profits improves trend-following systems of all speeds. Longer trends develop larger profits; therefore they were helped by larger profit-taking objectives. Faster trends needed smaller goals. Using a small profit-taking objective in a long-term system causes small profits and relatively larger losses; a large profit objective in a fast trending system was rarely reached.

Related Entries: Profit-Taking: Perry Kaufman (Test Period 1) | Kaufman Adaptive Moving Average (Setup & Filter) | Kaufman Adaptive Moving Average (Setup)

Related Topics: (Public) Trading Strategies

CFTC RULE 4.41: HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN LIMITATIONS. UNLIKE AN ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING. ALSO, SINCE THE TRADES HAVE NOT BEEN EXECUTED, THE RESULTS MAY HAVE UNDER-OR-OVER COMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH AS LACK OF LIQUIDITY. SIMULATED TRADING PROGRAMS IN GENERAL ARE ALSO SUBJECT TO THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFIT OR LOSSES SIMILAR TO THOSE SHOWN.

RISK DISCLOSURE: U.S. GOVERNMENT REQUIRED DISCLAIMER | CFTC RULE 4.41

Codes: matlab/kaufman/targets/